多元回归

以 multiple linear regression with two predictors 为例

$$\tilde{y}i = y_i - \bar{y},

\quad \tilde{x}{i2} = x_{i2} - \bar{x}2,

\quad \tilde{x}{i3} = x_{i3} - \bar{x}_3 .$$

important point:

In this model, as in many others, it is important to recognize that the model is an approximation to reality in the region for which we have data; including an intercept improves this approximation even when it is not directly interpretable

• Estimated regression models describe the relationship between the economic variables for values similar to those found in the sample data;

• Extrapolating the results to extreme values is generally not a good idea;

• Predicting the value of the dependent variable for values of the explanatory variables far from the sample values invites disaster.

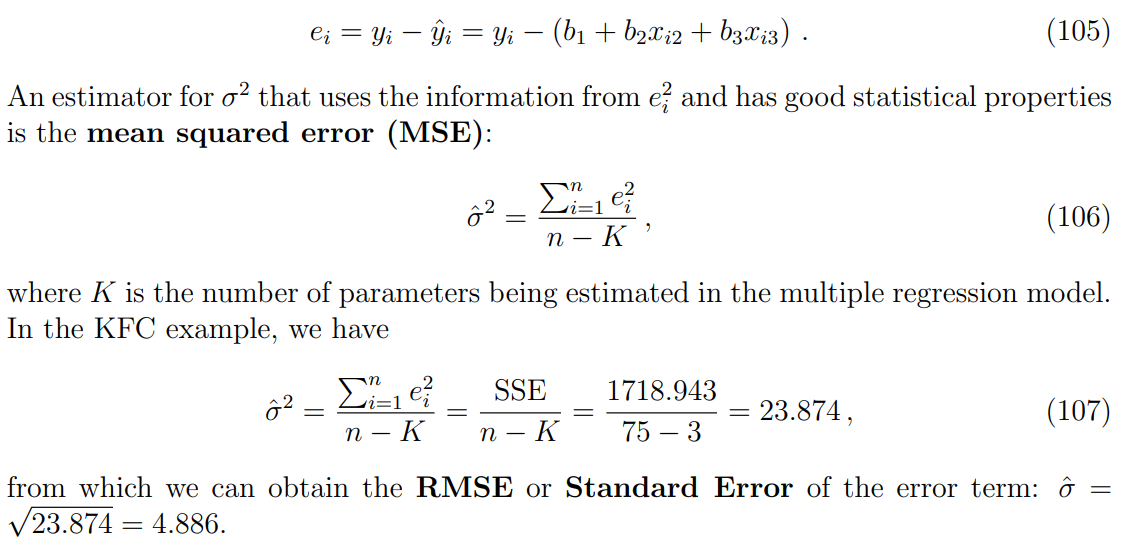

Estimation of the error variance

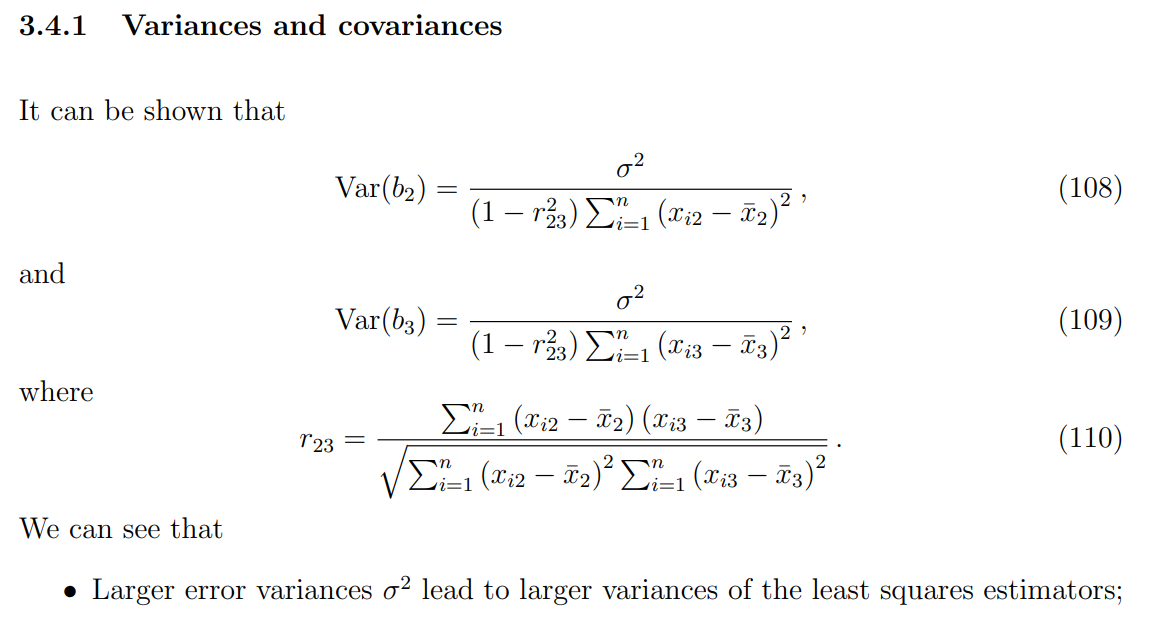

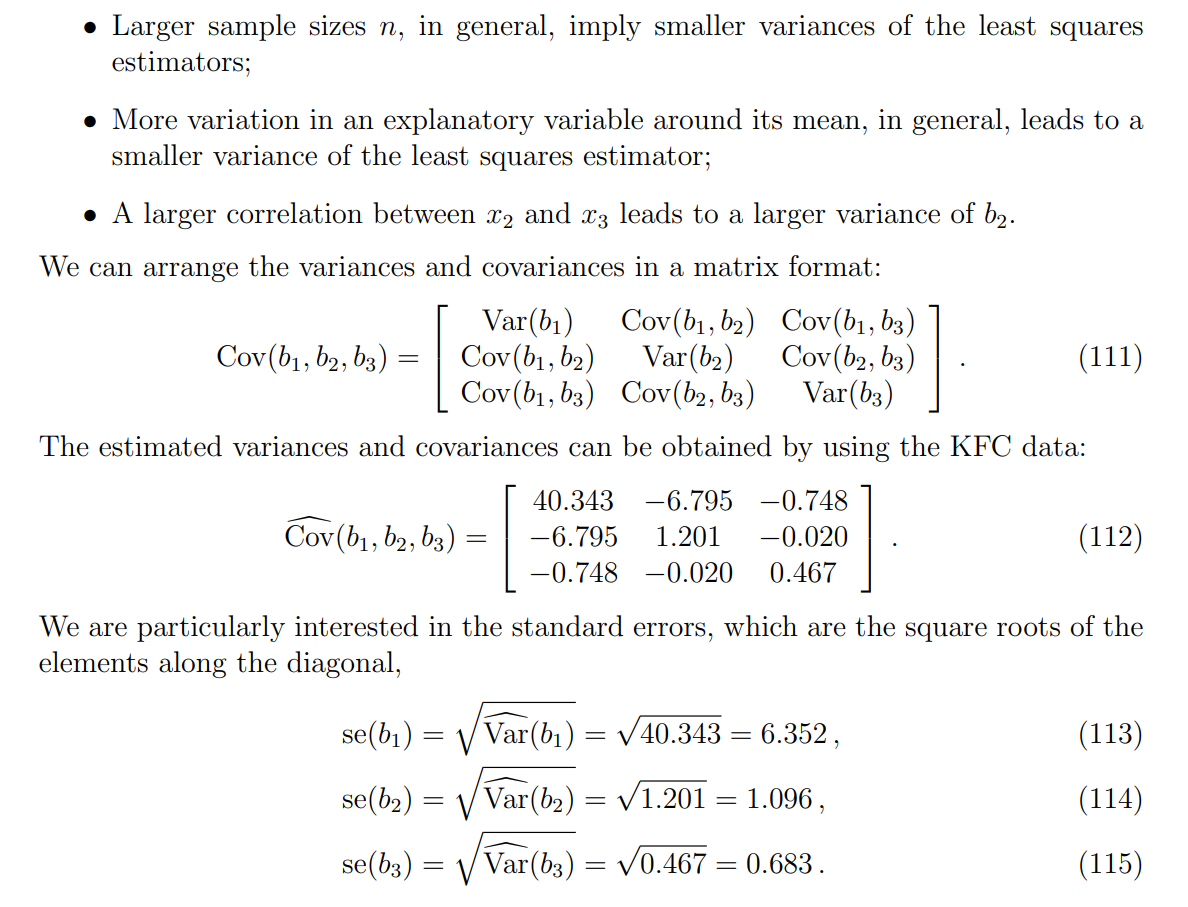

Sampling properties of the least squares estimators

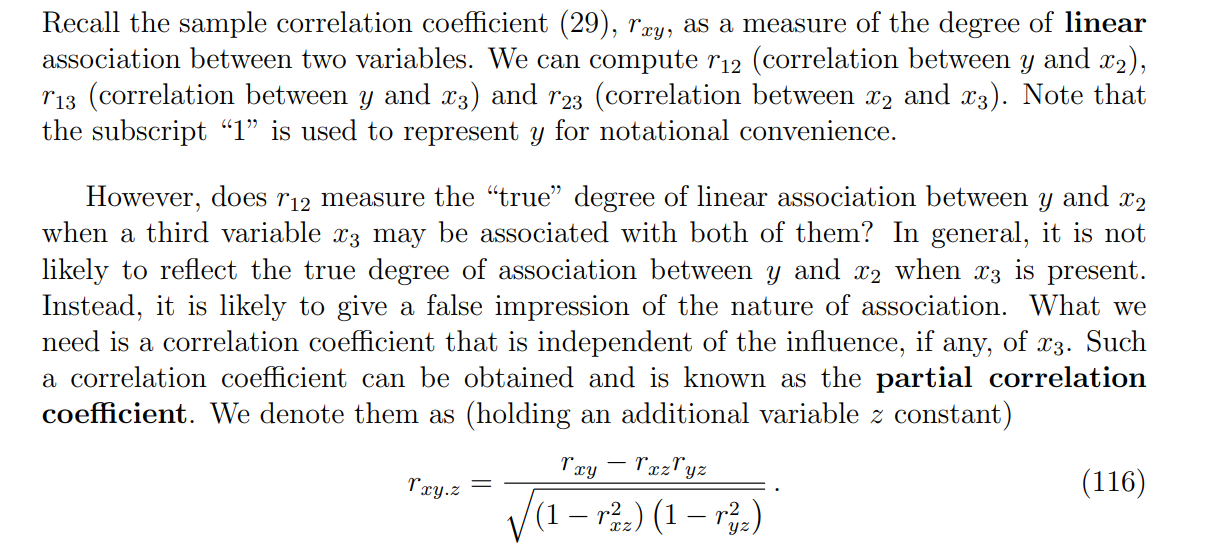

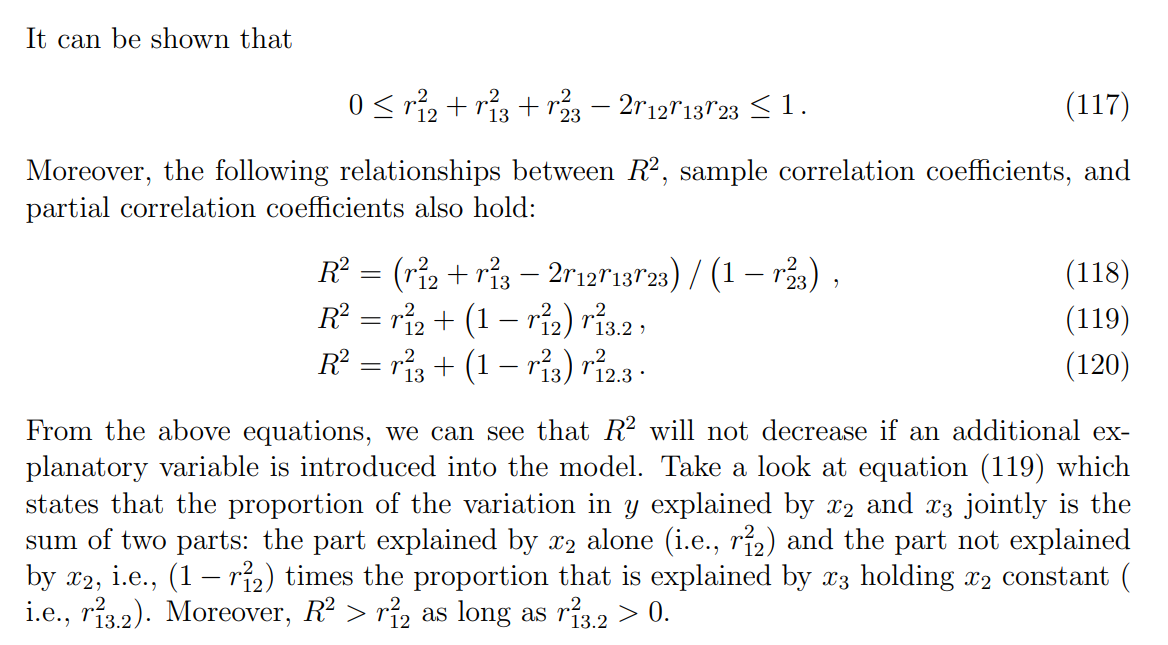

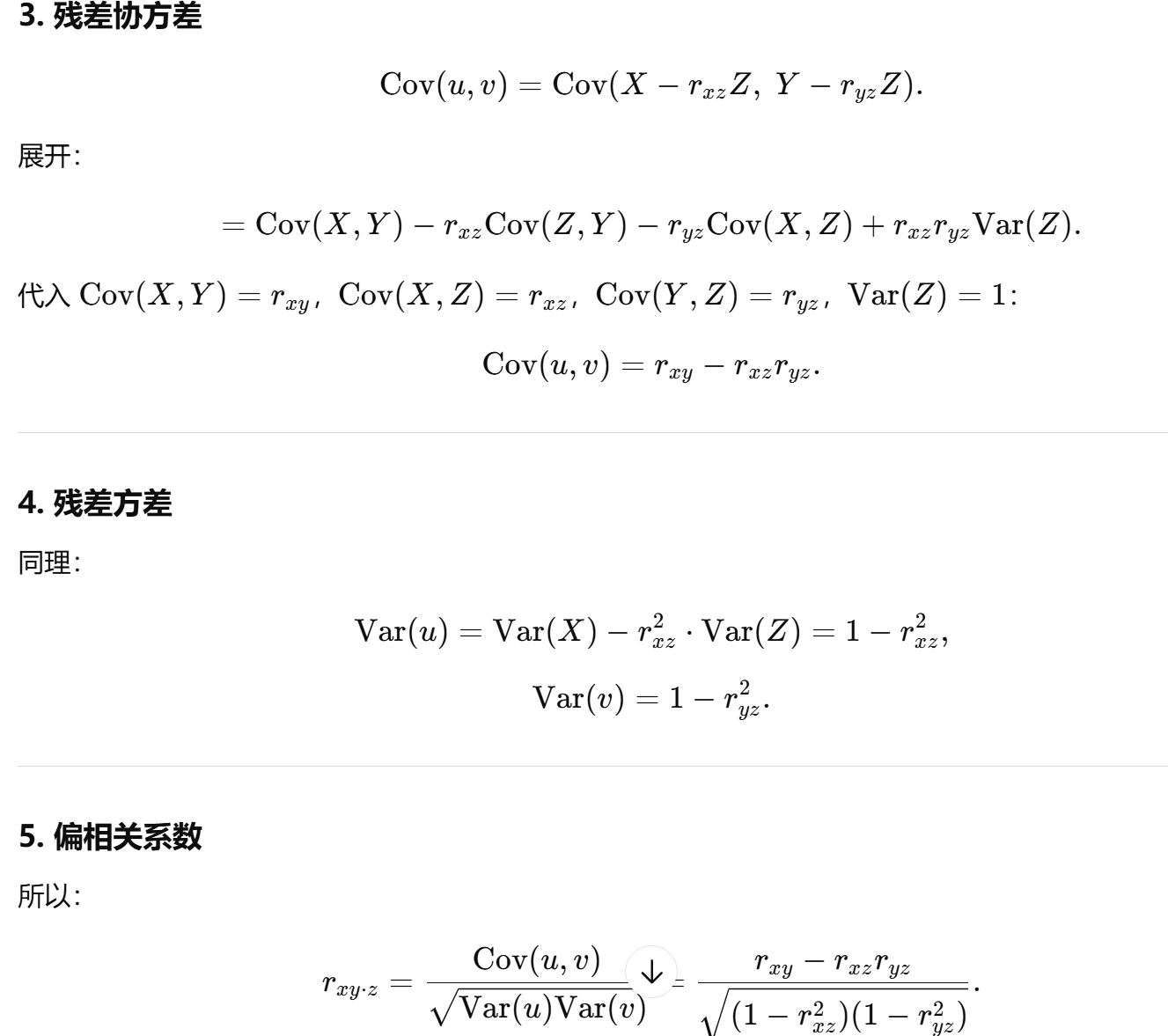

Partial correlation coefficent

标准化处理:

一开始就做了标准化处理:

那公式会极大简化。

回归系数更简单

回归 X 对 Z的系数:

因为 Var(Z)=1。

同理,回归 Y 对 Z 的系数:

残差形式

于是残差就是:

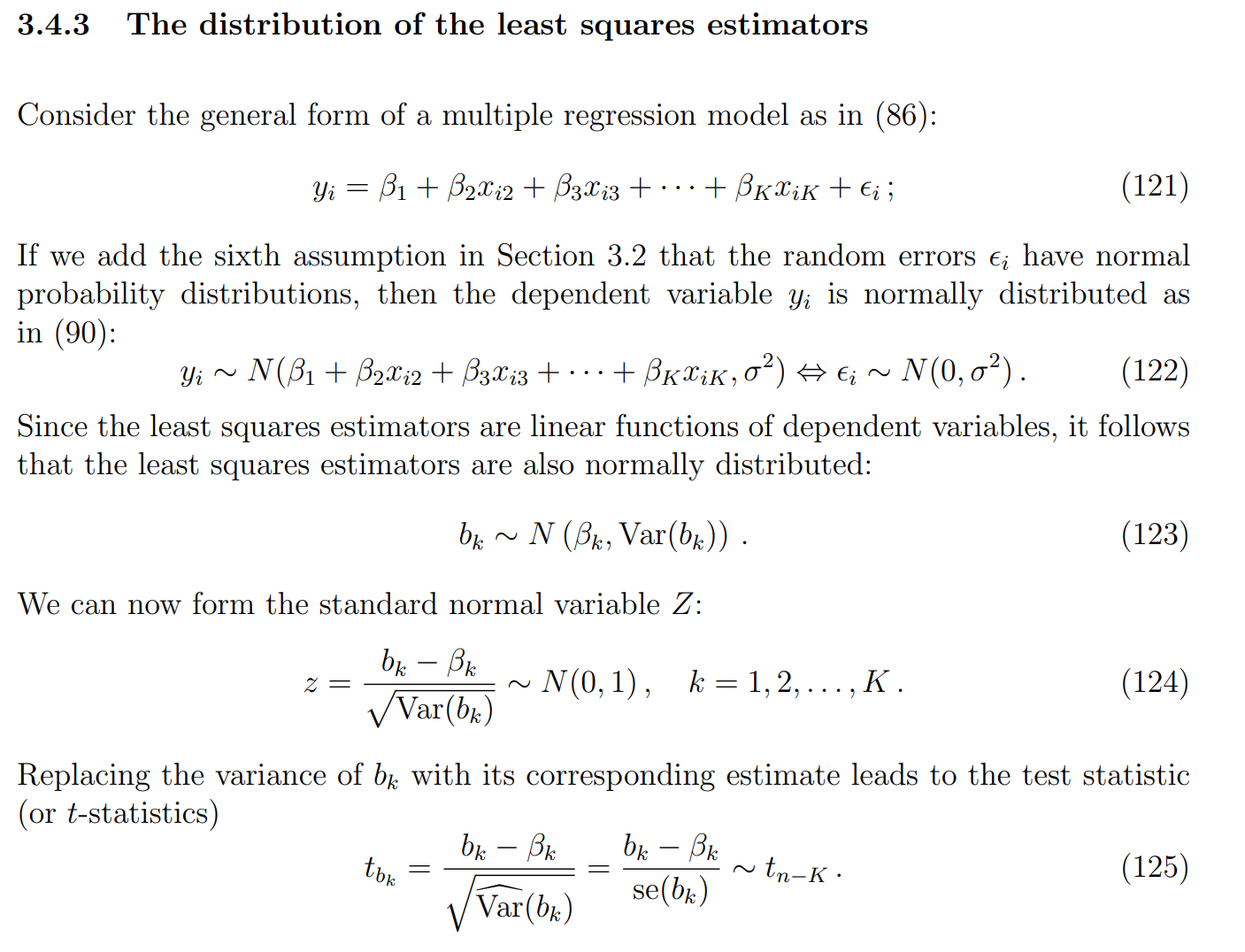

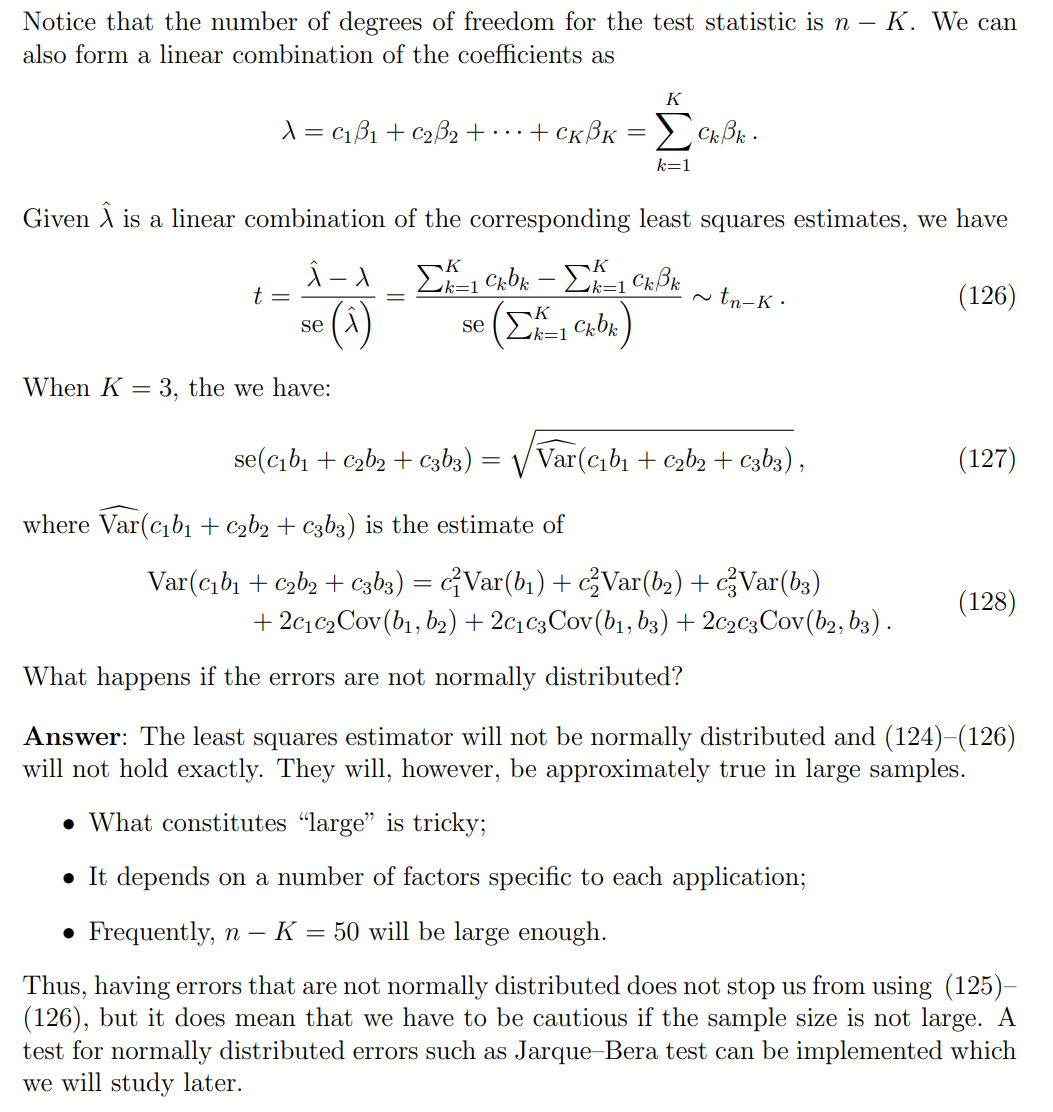

The distribution of the least squares estimators